Generally, a regressive tax is one where the tax burden is felt more heavily on the low-income, than on the high-income.

As conventional wisdom in “A” level Economics would have it, an indiscriminate consumption tax is likely to be regressive, especially in the absence of transfer payments to the poor.

The most common and easy-to-understand explanation is that lower-income households usually save less (and consume more) as a proportion of income, and therefore pay disproportionately more GST, than the higher-income households.

Of course, if it was that straightforward and in-your-face, then assertions by the Singapore Ministry of Finance wouldn’t have appeared bare-faced as some quarters may argue:

Analysing GST: The income-approach.

This is probably the more familiar of the 2 approaches that I will be discussing today.

The approach is simple enough:

- Evenly draw household samples across the income distribution;

- For each household sampled, measure the ratio of total contribution to GST annually against annual income;

- Attempt to find a correlation between annual household incomes and proportion of annual GST contribution against annual income: A negative one would point to the GST being a regressive tax.

This is the most common lay approach to understanding the impact of GST to the poor (and rich), especially with the recent furor surrounding the impending GST hike from 7 – 9%.

Its simplicity lends readily to intuition. Consider the popular argument that both the poor and the rich must consume somewhat similar amounts of necessities, since such goods offer little utility past the point of necessary consumption levels.

As a result, the rich have the added luxury of saving, unlike the poor who would have fully spent their income on necessities, which necessarily reduces the richs’ overall contribution to GST relative to income.

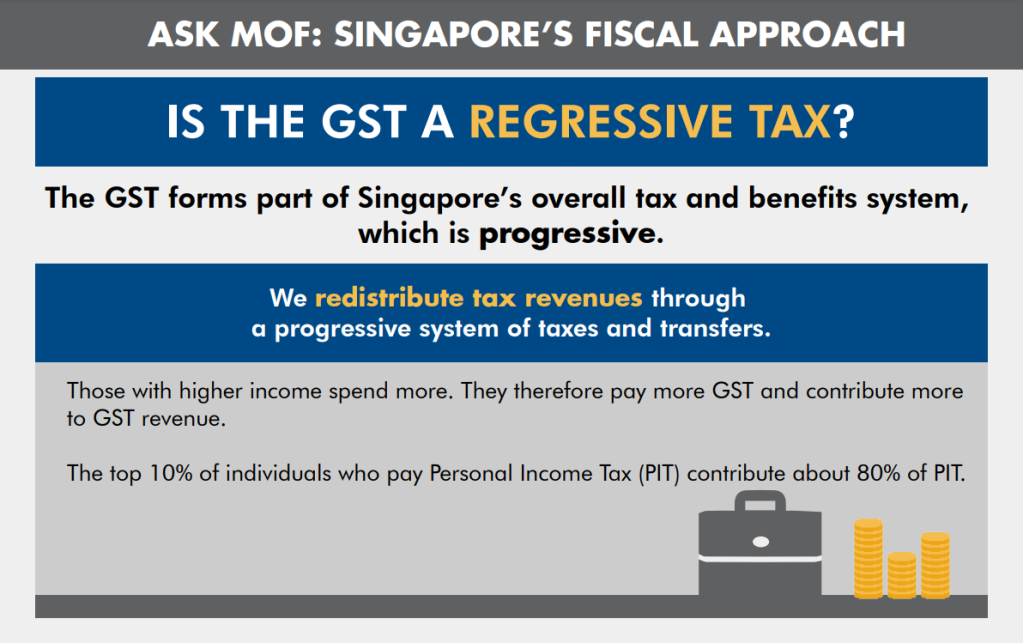

At the same time. the assertion from MOF that “those with higher income spend more” and therefore “contribute more to GST” ignores the generally accepted wisdom that a tax’s regressivity is measured by its impact relative to income levels, rather than in absolute terms.

At face-value therefore, it was personally difficult to take MOF’s argument seriously. And yet there might be more than meets the eye.

The expenditure-approach.

Perhaps unsurprisingly, there have been various arguments when it came to the methodology behind determining whether a tax is regressive.

A key complaint amongst many academics about the income-approach as above, has been how it is actually distorted by the savings behaviour.

Consider that one’s income is unlikely to remain at the same level across his/her lifetime:

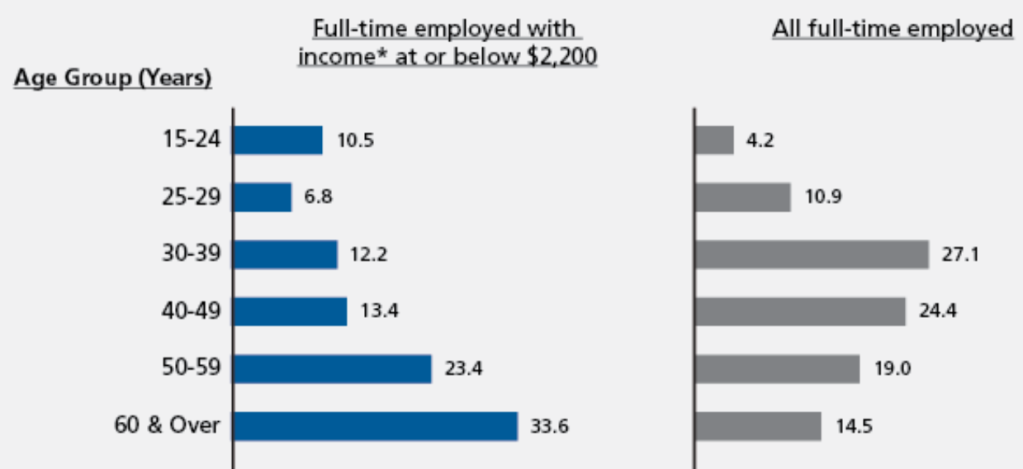

As can be seen, the share of low-income residents is over-represented by older workers. In this report from MOM, it was noted that these residents exhibit high-levels of home ownership, suggesting that destitution, at least, is not a foregone conclusion for them.

Extending these observations further, it is likely that a significant proportion of older workers have had their hey-days at work and accumulated significant savings for spending in their twilight.

Put together, the degree to which the GST is regressive, is likely to be overstated when counting GST contribution against income on an annual basis, as compared to over the lifetime, because:

- The low-income earners, whilst more likely to dissave now, may have saved in previous periods, overrepresenting GST contribution at present;

- The high-income earners, whilst more likely to save now, may dissave in later periods, underrepresenting GST contribution at present.

In an ideal world, we could remove the distortionary effect of savings behaviour by measuring the life-time GST contribution against life-time income across the population. Unfortunately, as you may imagine, that is easier said than done.

A more realistic, albeit imperfect workaround would be to utilise a basic graduates’ level Economics framework known as the Life-Cycle Hypothesis.

In its simplest form, it generalises the behaviour of consumers to one that plans for consumption on the basis of fully consuming the life-time’s income, in the absence of bequest motives.

This is basically formal-speak for a “rational” YOLO without fanfare, and often combined with another important Economics concept of Consumption Smoothing, which refers to the typical consumer’s tendency to attempt consumption at a stable level throughout his/her lifetime.

Putting the underpinnings of the Life-Cycle Hypothesis and Consumption Smoothing together, we can argue that the annual consumption spending can act as an imperfect proxy for lifetime income, allowing us to marry it with annual GST contribution.

It should be highlighted that this approach assumes that the GST contribution snapshot is reflective of lifetime consumption patterns, but as you may already have guessed, this may not always be true.

Nonetheless, this is still deemed preferable as “noise” when compared to bias associated with savings behaviour.

GST regressive? Or not?

For this section, I will be citing the findings from a particular study by Alastair Thomas: Reassessing the regressivity of the VAT.

For most part, the VAT is similar in concept to the GST and the study can therefore help shade light on whether the GST may be regressive as a tax.

Utilising the expenditure-approach and then mapping the VAT-Contribution-to-Consumption data against a composite poverty metric (to enable meaningful quantification of material standard of living), the VAT was calculated to be significantly less regressive, and even slightly progressive in countries that liberally apply exemptions on necessities.

Unfortunately, whilst the least regressive VAT implementations were observed to exhibit slight tax progressivity…it was really just that. VAT is for most part, still found to be regressive by nature.

And more unfortunately for us, Singapore’s GST is a non-discriminatory consumption tax, levied on all goods and services sold locally, with the sole exceptions of:

- Financial services;

- Digital payment tokens;

- Residential properties; and

- Investment precious metals.

But at the same time, businesses need not register for the GST if their taxable revenue doesn’t exceed S$1m. This means many mom-and-pop neighbourhood shops that many of us plebeians frequent for day-to-day stuffs are not subject to the GST, freeing us to an extent, from the regressive yoke of the taxman.

In the end, in the absence of studies made publicly available, and the dearth of analyses in the general Singapore discourse like this one, it is hard to say for sure just how regressive a tax the GST really is.

A big clue though, would be how transfer payments in the form of GST rebate vouchers have been a centerpiece to most, if not all manner of discussions involving the GST. There is even a sanctioned and dedicated website that brings you through everything you need to know about it:

The GST, on its own, is likely to be regressive in nature, and I would hazard an educated guess that there were economists in the Singapore government who have done good number work to derive the GST rebate amounts, given the government’s insistence on prudence. At least publicly, that is.

Final word.

The question of whether a tax is regressive, ultimately doesn’t fully answer the question of how it negatively impacts the impoverished.

The author of the study I had cited, Alastair, had said as much when he made clear that the marginal utility per dollar spent by the poor is likely higher than that of the rich. Therefore measuring the regressivity of a tax in dollar terms doesn’t fully illuminate the true impact of VAT on impoverished households.

Ultimately, the primary purpose of the GST is in providing a (very) broad-based source of tax revenue for the state.

That consideration is likely to take precedence over inequality concerns, and more so when considering how the GST rebate vouchers can be adjusted and dispensed to the populace on a flexible basis (when compared to attempting changes to the tax structure proper), to mitigate the GST’s regressive effects.