Singapore’s current account has been posting significant surplus year-on-year.

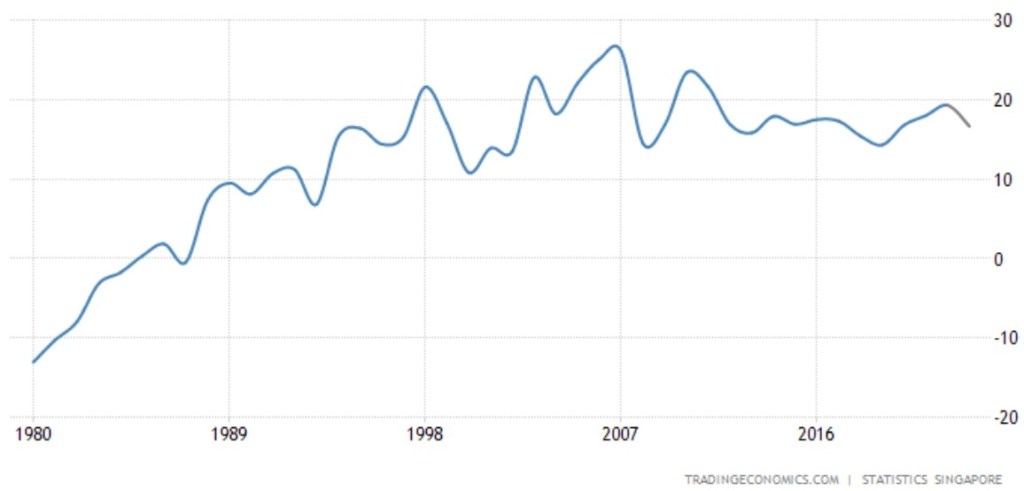

In fact since the 1980s, when Singapore’s current account began registering a surplus, it has been on an upward trend, reaching a peak of S$34+B in 2021.

Even after accounting for economic output size, the surplus as a percentage of the GDP showed an increasing trend as well, stabilising in the last few years at just under 20%:

It may come as no surprise that Singapore easily ranks amongst the top 10 countries globally for current account surplus size relative to GDP.

Still, it boggled my mind that even when considered in absolute terms, Singapore’s current account surplus was comfortably amongst the top 10 countries globally – which underscores how unusually large it really is.

The trade surplus argument.

The “standard” ‘A’ level and IB Economics texts would point to a balance of trade surplus as a starting point, which would imply very competitive domestic producers vis-à-vis foreign competitors.

That includes free notes provided by yours truly, by the way.

For those who require a primer to what the balance of trade, current account, and the broader balance of payments are, Khan Academy does a good job in explaining it:

By definition, the current account measures the net flow of payments relating to the goods and services trade, and the net flow of income from abroad.

In the vast majority of cases, the goods and services balances outweighs the income balances by a significant margin, and Singapore is little different in that respect, with the trade balance being nearly 80% larger than the income balance in absolute terms:

In fact, many schools have just about done away with the traditionally taught concept of “balancing the balance of payments” as a macroeconomic goal, advocating instead the balancing of the current account as a solid long-term goal.

The reasoning behind that lies with the understanding that the current account balance must be offset by the capital and financial account balance, which involves the net sale of assets to/from abroad, to maintain equilibrium to the domestic money market.

Accordingly, a current account surplus must therefore mean an outflow of money to purchase assets overseas, whilst the opposite is true for a current account deficit. And whilst the latter is typically deemed more undesirable, as we will see later, a persistent increase in ownership in foreign assets may not be great either.

If the goal is therefore to maintain a balanced current account, and the trade balance accounts for the majority of the current account balance, it stands to reason that aiming for a balanced trade balance would be a reasonable proxy goal as taught in many schools nowadays.

An undervalued SGD?

In a free foreign exchange market, conventional economic wisdom holds that the currency’s external value would stabilise at a level where the current account is balanced. This is due to:

- The currency appreciating with a current account surplus causing the surplus to diminish; and

- The currency depreciating with a current account deficit causing the deficit to diminish.

The explanation behind these currency movements is best understood with the application of the Marshall-Lerner Condition, which I had previously elaborated on here.

In short, such theories imply that Singapore’s persistent (and growing) current account surplus must be due to the SGD being undervalued as a managed-float currency. The Workers’ Party Economics Wunderkid, Jamus Lim, alluded to that as much in a parliamentary exchange last year with the Minister of State for Trade and Industry Alvin Tan.

There are costs associated with a relatively weak currency.

For example, the cost of imports would be higher, and given Singapore’s reliance on imports for much of the final goods and services, this increase in cost would be passed on to consumers. This is on top of the expansionary effect on the aggregate demand due to a better net export performance, which further induces price inflationary effects.

And although Singapore’s exporters should benefit in price competitiveness brought on by the weaker currency, they import much raw materials, so that production costs get driven up, and at least negate some of the improvements to price competitiveness.

Worse, the unusually large current account has attracted attention of the wrong kind, most recently in 2019, when the US Treasury added Singapore to a “watch-list” for currency manipulation.

Needless to say, the Singaporean top-dogs were compelled to refute, which leads to another interpretation of the current account surplus.

Excess savings vis-à-vis investments locally.

It will probably be a stretch to the layperson that the “strong” SGD is in fact, undervalued. And the Communications department of MAS would have you agree too, citing the very same issues associated with having a weak SGD as discussed above.

Of course, an alternative explanation had to be served at that point, which comes duly in the expression of the current account as the difference between national savings and investments in Singapore:

Current Account = S – I

For a detailed explanation of its derivation, check out my previous article here.

A current account surplus here, can then be interpreted as S > I, implying an excess of national savings over investments (foreign and domestic) in Singapore.

Here’s MAS’ explanation of how we got there:

- “National saving has grown in line with rising incomes” and “Singaporeans stepped up saving for old age“;

- “Singapore has a fully-funded, defined contribution pension scheme called the Central Provident Fund (CPF) in which Singaporeans save for retirement and medical needs“; and

- “The government had deemed it prudent from the beginning that Singapore diversify some of its saving abroad“.

And here’s how contrarian views offered look like respectively:

- National spending has not grown, especially on social aspects, sufficiently fast enough to assure people of a comfortable retirement;

- Singaporeans save excessive amounts due to regulatory duress; and

- There’s a relative dearth of investment opportunities in Singapore.

Is a current account surplus bad?

The overall picture is decidedly mixed for several reasons. We can see that by turning now to the likely motivations for maintaining the surplus.

Looking first from the perspective of the SGD having what MAS doesn’t explicitly deny to be an upward pressure on its value (it can’t deny away the S$400B foreign reserves accumulated through exchange rate interventions), there are reasons to believe it is a product of prudence.

Firstly, allowing the upward pressure on the SGD’s value to persist makes for easier (and therefore more predictable) monetary policy adjustments:

- A contractionary adjustment in response to overheating, commonly due to better global market performance, can be done by simply allowing the relatively higher demand for SGD to filter through; and

- An expansionary adjustment in response to deflationary pressures, commonly due to poor global market performance, can be done by accumulating foreign reserves (selling more SGD), which is hardly the worst kind of intervention.

Secondly, currency stability and a persistent upward pressure on the exchange rate that is allowed to filter through slowly, tends to foster good investor sentiments, which also encourages a virtuous cycle, in that good business confidence frequently begets more of it.

Whilst an excess of savings over investments in Singapore may for one, indicate scope for more spending to improve societal welfare, prudence (as opposed to slaying sacred cows) dictates that opening the spending spigot may prove more difficult to close later, and should be approached with caution.

On the other side of the same equation, having an excess of savings to be invested outwards can also be seen as a “happy” problem as having the opposite problem leaves the country at the mercy of foreign investments.

Do you see a common thread to the arguments in favour of maintaining a current account surplus for Singapore? I think I do, and it’s “conservatism” that came to my mind.

Whether you think that’s the problem of choosing to maintain the surplus will ultimately decide then, whether you think that Singapore’s persistent current account surplus may prove a liability, especially in the longer term.